If you have been following financial media, you might have come across the failure of a travel company called Thomas Cook. 600,000 British citizens were left stranded overseas, tens of thousands of employees left hanging, and perhaps hundreds of hotels, resorts, airports were left holding the bag for Thomas Cook shareholders and managers.

Before Monday 23rd September 2019, I didn’t even know who or what Thomas Cook was. After Monday, it is easy to ride on the wave of media bashing and predict the past. Let’s try to enjoy some good-old-hindsight-investing and rationalize what happened.

The Case

First and foremost, a company must be profitable before I invest in it. I don’t like to participate in speculative bets unless the reward-risk payoff is huge. Let’s say I could time travel back to 2014. A quick look at the operating performance of Thomas Cook gives it an acceptable grade.

The company makes positive operating profit (i.e., gross profit) almost every year in the last 10 years, except for an anomalous 2012. The profits are fluctuating definitely, but it isn’t too bad. Some of my current holdings have graphs that look like this or worse. On average, this company makes roughly 200M pounds a year in gross profits.

However, gross profit only measures the profit from making and selling widgets (or services in this case). It excludes things such as interest costs and taxes. If you looked at the net income (which is a more complete view) in the graph below, it is truly horrible. The company has lost money every single year. At this point, I probably would have stopped the due diligence. However, for completeness of the analysis, let’s continue.

The company’s Free Cash Flow seems to look decent. In some companies, you can lose money because your properties “lose market value” and you have to record it into your financial statements. However, the operations can be profitable and spit out Free Cash Flow annually. REITs are an example of entities that sometimes behave like this. Could it be that things are not as bad as it seems? Let’s take a look at the financial health of the company then.

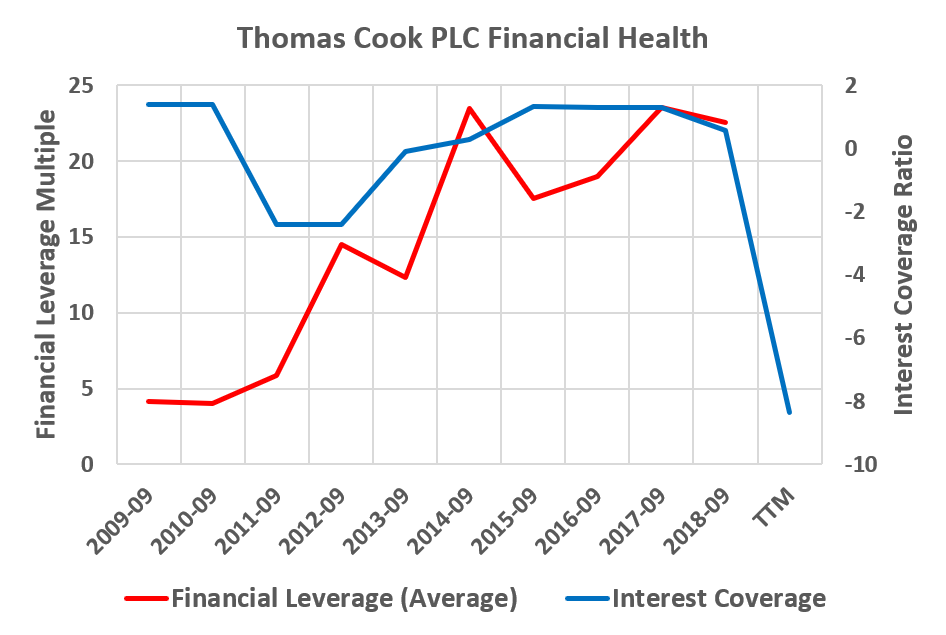

Free cash flow alone is not enough to see the full picture. We need to look at the financial leverage ratio which was around 5 times in 2009. That means it started off roughly as leveraged as an average home-buyer in Singapore. When you put down 20% down-payment on a house and borrow 80%, your leverage ratio is 4 times (80% / 20%). Thomas Cook’s leverage of 5 while not exactly pleasant, is not a red flag.

However, what happened in the next 10 years is an absolute nightmare. In the “good” years, the company had a 300M pounds of operating profit, but it could not even cover interest payments. In case the numbers are too big and mind boggling to you, I can put it in individual terms. It is like having an annual income of $50,000 from your job but having credit card debt of $300,000. The annual interest payments alone are above $60,000, more than your salary. You will slide towards bankruptcy unless you find a way to increase salary and restructure your debt.

For Thomas Cook, the leverage goes from 5 to God-knows-where22. If I had been an investor in this company in 2009 for some reason, I probably would have sold some time in 2012 or 2013.

Speaking of selling, the last step in an investment decision is to look at the market price. Let’s take a look at the company’s stock price history, complete with all the technical indicator sorcery.

Here, we see the stock price action of a company in a death spiral. In case you don’t want to zoom into the price chart, the stock price of Thomas Cook fell from 250 GBP to 3.45 GBP across the last 10 years. This week, it went into liquidation and the trading of its stock has been suspended. It should be roughly worth 0 in liquidation value.

I must admit, declaring that I will sell in the past is like playing a game with cheat codes. Even when I cheat with my time-travel-investing-powers, I would have still suffered a devastating loss of 60% to 80%. Perhaps laziness and inaction may help me recoup a bit more money if I had been slower and sold in 2014 when the price went up. Nevertheless, from 2013 and beyond, the interest coverage ratio is a massive warning sign to get out while other investors choose to turn a blind eye to the mountain of debt.

Why the company paid dividends in some years absolutely baffles me. Perhaps it is like someone neck deep in credit card debt. It makes no difference whether or not he picks up the bar tab for everyone after one final night of partying because he has an appointment at bankruptcy court the next day anyway. This leads me to a few lessons for myself and fellow readers.

Lesson 1: I should monitor Personal Debt and Interest Coverage Ratio

As individuals, we should never put ourselves in situations like this. I don’t risk what I have to try to earn what I don’t need. Thomas Cook got itself into this situation by borrowing tons of money when times were good and went on acquisition sprees.

Some property investing “trainers” tell us to leverage up on multiple properties, or even worse, inflate valuations to get cash back on loans to have effectively zero down-payments. When times are good, their advice makes us a lot of money. This produces an illusion of control over economic forces beyond any single person’s control. The problem is, nobody knows when bad times will come along.

Doing it when my salary can cover my installments puts me at some risk of foreclosure in the event I lose my job. If I have a big pile of cash sitting behind to service the debt for a year or more, I am somewhat safe though life can get uncomfortable. However, if my plan is to depend solely on the tenants for the loan repayment, things can get very ugly very fast. This is especially true if the asset value backing the loan is correlated to the cash flows from rent.

If you plan to do this, I have to warn you against it. During good times, the trainers cheer and celebrate with you. When things get ugly, the trainers probably will close shop and disappear. You won’t be alone however. I will be there with you perhaps to lend some moral support and more importantly, for the fire sale.

Lesson 2. I Should Monitor My Investments’ Financial Health

Let’s say in 2009, I bought this company because of some random “growth-stock-must-be-good” story. Perhaps I thought the growth potential in travel agency industry is big. Much as I trust the managers, I should check in at least once a year on how the company is doing. After seeing not 1, 2, 3 but more number of years of worsening financial health, it should be time to sell. Whether I made or lost money is inconsequential at that point.

Instead of hiding behind the words “paper-loss” or “long-term investment”, every year when I review investments, I try to view it from the perspective of a fresh investor. This means if the company is not good enough for new money injections, it is not good enough for old money to stay there.

Lesson 3. Price Movements Can Be Irrational

By 2018, looking at the data, it has become clear this company is going towards bankruptcy. As for the buyers at the time, I truly cannot understand what their thinking process was. I can only guess they didn’t do any due diligence.

If you depend on the market to get a sense of what the value of something is, you can get a generally correct answer most of the time. However, the market can become very irrational as we see in this case. It can be dead wrong for extended periods.

Even when you spot such companies, I don’t recommend shorting the stock or buying OTM put options on it too unless you are very clear what you are doing. The market took 6 years to recognize this company is a cash furnace. The market may stay irrational longer than you can afford to pay the OTM option premiums.

Lesson 4. Insure Against Catastrophe

Buy insurance to hedge against doomsday scenarios. As travelers, you should consider getting travel insurance to insure against such events. A delayed flight or cancelled holiday hardly counts as catastrophe so perhaps you can choose to ignore this part.

Hospitalization and major illnesses are totally different animals, however. I suspect an exploding medical bill is the main reason why financially responsible people fall into financial hardship. Buy at least some insurance to cover yourself from uncapped medical expenses in the event you fall sick.

Too much of a good thing can be a bad thing though. I don’t recommend life insurance or investment linked plans and I say this despite having vested interest in more people buy insurance plans due to my Great Eastern stock. The only reason you should buy life insurance or ILPs is if you absolutely have no idea how to invest and don’t wish to learn. If you do buy them, I respect and understand your decision and humbly thank you for your business.

Lesson 5. Some Diversification Is Safe

When Worldcom and Enron collapsed, their employees lost everything. Right now, the situation is not very clear. Some Thomas Cook employees may be able to hold onto their self-contributed pensions. I don’t know the situation as things are still in flux.

If you are an employee in a firm that gives you stock, this episode is an important learning point. Try to ensure it is a small part of your whole portfolio. It is good practice to decouple your active income and passive income/investments.

Apart from employer specific risks, you also have to keep your eye on own-country bias in investments and income. While I am lucky to be born in a stable country like Singapore, our country is always one US presidential tweet away from massive pain. I can’t tell you how much to spread out your bets, but at least diversify a little bit at the minimum.

Conclusion

My wife suggested this title and I thought it was quite funny. Jokes aside, let’s not forget what we saw this week was a live example of how uncontrolled debt and burying your head into the sand can backfire spectacularly on a massive scale. 600,000 innocent customers and ten thousand employees have to suffer real, negative impacts on their lives.

I have unpleasant opinion about the people who let this happen but going there will be ranting. I would like to let Thomas Cook shareholders, employees and customers have the dubious honor of doing the talking on my behalf.

Stay safe in your investments.