Tom was a little short of money and he owes his landlord rent from last month, $1000. Mr Landlord was fuming when he comes looking for Tom. Tom asks for permission to delay it but Mr. Landlord offers him a really strange proposition. He gives Tom 2 options.

Option A: “Tom, if you pay me $1000 by the end of this week plus $10 dollars for making me come down here, you can continue staying here. Otherwise, I will kick you out of the house right now as per the contract,”

Option B: “If you really cannot afford it but don’t mind paying me for a longer period, we can negotiate to stretch the rent over a longer period. Take it that I loaned you some money. You just have to pay me $0.10 today, $0.20 tomorrow, $0.40 the day after, and the amount keeps doubling every day. You can take your time, but we can sign a new contract if you prefer this. You won’t ever have to pay the $1000 a month plan if you sign up for this new plan. Don’t worry, I won’t kick you out unless you owe me a million dollars!”

“A million dollars? How can rent possible hit a million?!” Tom was amused and laughed. Mr Landlord laughed along and simply said “Yeah no way, so you probably can stay here for quite a while! Don’t miss this deal before I change my mind!”

If you just eyeball the numbers, Option B seems to be really attractive. 10 cents! 20 cents! Tom thinks so too. “Those numbers sure look dirt cheap and can live in this place forever! He is so stupid.” Tom thinks Mr. Landlord just gave him a ridiculously great deal and signed up for the new plan without much thought.

Is Option B such a great deal? Let’s do the hard work of looking at the numbers.

Day 1: $0.10 Day 9: $25.60

Day 2: $0.20 Day 10: $51.20

Day 3: $0.40 Day 11: $102.40

Day 4: $0.80 Day 12: $204.80

Day 5: $1.60 Day 13: $409.60

Day 6: $3.20 Day 14: $819.20

Day 7: $6.40 Day 15: $1638.40

Day 8: $12.8

By day 15, the daily rent exceeded what Tom was paying monthly. You can keep doing the calculations, but here are some landmarks.

By day 21, the rent would be $104,857.60.

By day 25, the rent would be a staggering $1,677,721.60. Mr Landlord shows up on the day 30 to wish Tom good luck and kicks him out.

This little anecdote is adapted from a story about rice and chessboards. I think the old story illustrates 2 very important lessons about managing finances, so I adapted it for a modern day example.

Money Management Lesson 1: If something is too good to be true, it probably is.

This lesson is probably the most important lesson of investing. If something is such a good deal that it is impossible to believe, it is very likely impossible. You have to be especially alert. If Tom had done his homework with the numbers, he would have realized how crazy the numbers would have looked by day 14. He trusted Mr. Landlord easily and signed up for a sucker’s deal.

Take a look around you. Do you know anyone who fell for a cryptocurrency scam? Do you know anyone who told you of a stock that absolutely was going to skyrocket through the roof? How about anyone who said you won in a lottery you have to pay a fee to claim your winnings? And closer to home, did any insurance agent try to get you to buy an endowment plan and showed you nice graphs of market-beating returns? The key lesson is – you absolutely have to do the homework to figure out good deals. Nobody will just give you a free ride.

Money Management Lesson 2: Compound interest is mind boggling and our brains are not capable of visualizing it.

Compound interest is a very scary thing. In the short story about Tom, he was on the hook for a rent that compounded 100% daily. The starting amount was very small, but the effects of compounding grows very large very quickly.

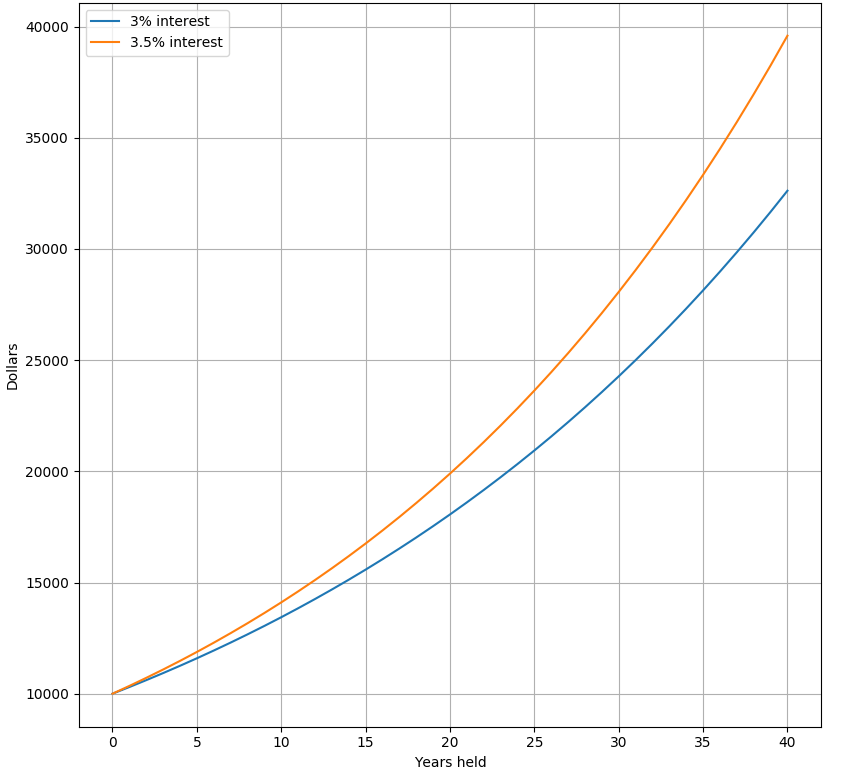

In mathematics, the calculations to figure out compound interest is called a geometric progression. It gets very big very quickly. The humans brain is not well equipped to deal with this effect. To show you why, let’s pretend we have the following scenario. Singapore’s government issued 2 different government bond with the following characteristics.

Bond A gives you 3% returns a year, can be converted back to cash in 1 month.

Bond B gives you 3.5% returns a year, minimum holding period is 3 years

You realized you have $10,000 of savings and want to invest them. Of course you know Bond B is a little better than Bond A, because the interest is a bit higher. Is the difference of 0.5% really just a little bit higher? Let’s plug the numbers into a calculator and figure that out.

At the end of 40 years, the difference between the 2 bonds is $6,972, a full 69% difference on your original investment.

What if you saved $10,000 every year and invested that extra money into these bonds? The difference is massive.

At the end of 40 years, the difference is a staggering $98,462. By choosing the investment plan that was “only a little bit better”, you are ahead by almost 10 years worth of savings. That has very real effects – you can choose to quit and not argue with morons in the office, or you could retire a full decade earlier to spend time with your family.

While Tom’s story is slightly exaggerated, it is an illustration of compound interest’s real life effects. In Singapore, credit cards have an interest rate of roughly 25%. If you choose to use credit cards, please do not ever forget to pay the balance off every month. Before you swipe for that trip to the Maldives or home remodeling, ask yourself if you can pay off the balance immediately when the bill comes. If you can’t pay the balance, you can’t afford it. Don’t do it. Don’t be like Tom.

To end this post, I quote a famous physicist on this topic.

“Compound interest is the 8th wonder of the world. He who understands it earns it. He who doesn’t understand it pays it.” – Albert Einstein

Save, invest, and watch it grow beyond your imagination. Cheers.

One thought on “2 Powerful Lessons about Money”