One of the companies that I am happiest to own is Taiwan Semiconductor Manufacturing Corporation, abbreviated as TSMC. I reviewed the company’s financials recently and would like to talk about it here. The company is listed in Taiwan and the US with tickers 2330 and TSM respectively.

Company Background

TSMC is in the business of semiconductor fabrication. You probably use a TSMC-made product without knowing it – your phone, computer and television set probably contain parts made by TSMC. If you have an iPhone or drive a modern car, chances are you are an end customer of TSMC.

So what exactly does TSMC produce? It buys raw silicon wafers and puts them through special lithography steps in their fabrication facilities (fabs). By the end of these steps, the wafers become tiny electronic chips. These chips are then put into end products by TSMC’s customers.

TSMC is currently using its 5 nanometre process to build chips. That means each individual component (also known as a transistor) in the chip is just 5nm in size. 5 nanometres! To put that number in context, one strand of your hair is 100 micrometers thick. You can fit 20,000 of those tiny things across one strand of your hair! This means smaller and more powerful phones and computers.

I am an engineer who knows this field quite well but it always amazes me how much human civilization has advanced just by watching the progress made in the semiconductor sector. How TSMC makes its stuff is too complicated to cover here. If you are interested, you can look up Wikipedia’s page on what a semiconductor foundry is. What I want to examine is the industry as a whole first, then talk about TSMC in particular.

Semiconductors are quite peculiar. Why do the companies come in all shapes and sizes?

Competitive Landscape (Verticals, Designers, Fabs)

In the past, all semiconductor companies were vertically integrated. That means they did it all – designing the chips, fabricating them from raw silicon wafers, and marketing the end products to customers. Such semiconductor companies still exist – Intel, Micron and Texas Instruments come to mind readily.

Unfortunately, the business of manufacturing things has high capital expenditure requirements. As a consequence, a generation of new-age design firms were born. These companies’ business models are to just design and sell their products. They pay someone else to fabricate their designs. Nvidia, AMD, and Qualcomm are 3 such examples. AMD is an interesting case. It used to own fabs until about a decade ago, when it decided that the costs of maintaining their own fabs were just not worth it. AMD exited the fab business, selling its fabs to a new company called Globalfoundries.

TSMC and Globalfoundries are the fabs, also called pure-play foundries. They purely manufacture chips for their customers and do not try to design their own chips. Their role is to ensure they can manufacture the smallest and most advanced chips in the industry. In order to do so, they conduct a lot of R&D and invest in expensive equipment to implement the new processes. TSMC is currently leading the pack, with the smallest transistors. This “leading” is better described as “crushing it” – even though multiple sources disagree on the exact figure, they all agree that TSMC’s market share is roughly 50%, more than the next 5 competitors combined!

With that broad overview done, let’s zoom in on TSMC’s data. Here are the things I care about the most. A word of caution before you proceed – 1 share of TSM if equals to 5 shares of 2330, so don’t get confused when you do your own research.

Here is my investment checklist.

(A) Is the Company Profitable?

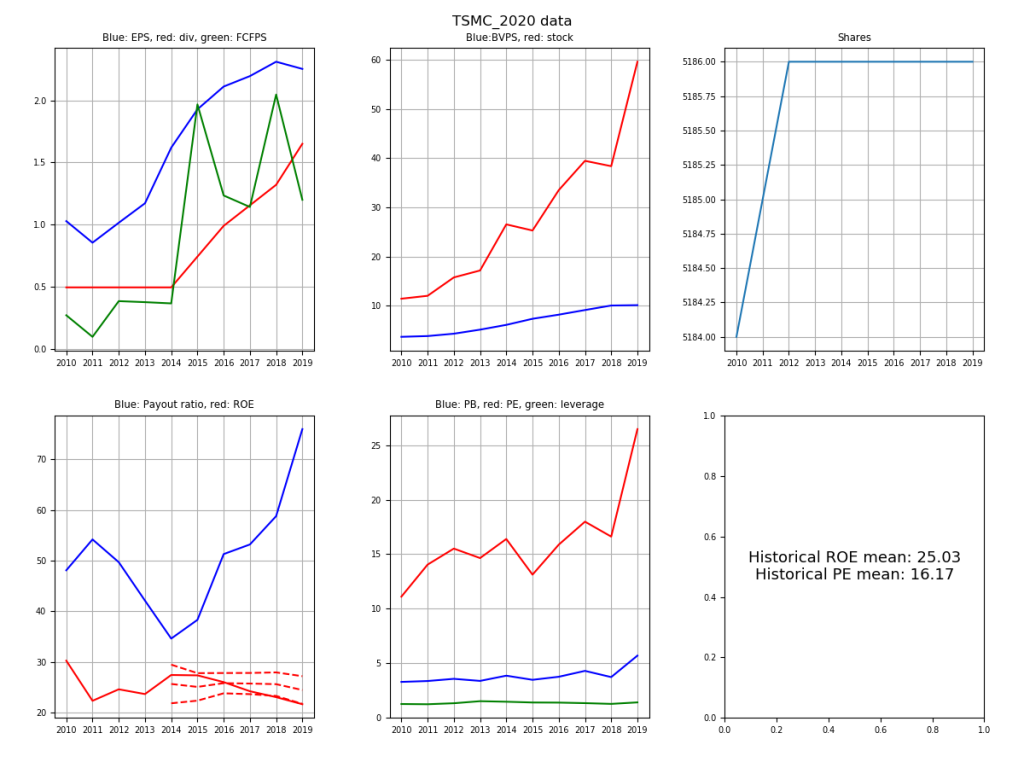

This is a straightforward yes. The company exhibited profits every year in the last decade. Their profit levels weren’t stagnant either, the earnings per share actually grew from $1.00 to $2.20 in 10 years (blue line, top left graph).

(B) Are the Profits Real?

Based on its financial statements, TSMC is really profitable. However, its competitors languish far behind. Here’s the trailing 12 month data for some of the biggest pure-play fabs/foundries.

| Company | Gross Margin | Net Margin | Return on Invested Capital | Return on Equity |

| TSMC | 48.5% | 35.25% | 21.16% | 23.96% |

| UMC | 17.2% | 5.80% | 3.76% | 4.36% |

| SMIC | 22.5% | 8.21% | 2.62% | 4.46% |

| Globalfoundries | Private | Private | Private | Private |

When I first looked at this table, I was suspicious of accounting gimmicks. As a whole, the data confirms my view that fabs are notoriously poor investments, so TSMC’s picture seems really anomalous. Could it be too good to be true?

In order to check whether there is any funny business going on, my first step was to look at the company’s book value. In 10 years, the company retained ~$8 of profits and reinvested the money. During this same time, TSMC’s book value increased by $7 (top middle, blue line). By this metric, the business seems to be doing OK, especially after you consider some depreciation of assets over time.

My second step was to inspect the ROE of the company (bottom left, red line). As the book value increased, the ROE fell a little, but was still within the range in the last decade. TSMC managed this despite maintaining a constant level of leverage (bottom middle, green line), so I think no funny business is going on. I gave the company some leeway – after all, the crypto-currency mining market collapse of 2018 and Trump trade war hurt semiconductors, so I could excuse some fall in ROE. Usually, this is enough to pass my are-the-profits-real test. However, I was extra cautious with TSMC since its results are extraordinary as compared to its competitors’ data.

My final step was to look at the dividends (top left, red line) over time. It increased from $0.50 to $1.60. The last time I checked, dividends that goes into your bank account cannot be faked easily.

TSMC passes my smell-BS test.

(C) Are the Profits Sustainable?

In the short to medium term, the profits are definitely sustainable. This takes some understanding of the semiconductor business.

When a customer like Apple wishes to order CPUs from TSMC, TSMC sends the customer a software called a product design kit or PDK. This is a software tool and contains all information a designer needs about TSMC’s manufacturing process. With this information, Apple will design a CPU and send the finished design back. TSMC will then churn out millions of units of that design.

This means in the short run, customers are stuck with TSMC. Any customer cannot move its designs to a competitor quickly because the different fabs have different manufacturing lines and PDKs. It takes an entirely ground up design process to migrate a designed product to another fab.

In the medium term, the profits are sustainable as long as TSMC continues to lead in advanced technology. Currently, no pure-play fab company comes close to TSMC’s position. In 2019, one of the largest competitors, Globalfoundries, announced that they gave up trying to chase TSMC to make the smallest chips.

If we also consider not-entirely-pure-play fabs (e.g. Intel and Samsung) who do also fabricate chips for customers: these fabs are reasonably close in technology but they suffer from other problems. Intel is hopelessly behind in terms of building power efficient chips (just try to benchmark AMD vs Intel CPUs and you get what I mean). Samsung is probably able to do it pretty well but customers are likely to be worried about Samsung’s other business divisions having access to their designs. For instance, if you are making a special LED chip for computer monitors, how can you ensure that Samsung doesn’t study your design for their own television business?

So far things are rosy for TSMC. However, there is a threat to profits in the 10-year-and-beyond time frame. The Trump trade war has revealed a strategic weakness in China in that she is too dependent on the US for advanced semiconductor parts. To mitigate this, China’s government has increased state investments into the semiconductor sector. Google “China IC industry fund” to see related content.

On top of potential competition from China’s state-backed companies, there is the threat of China-Taiwan reunification turning into a ugly shooting match. Most of TSMC’s plants are based in Taiwan, so there is no way to diversify away this risk.

I am confident of short to medium term prospects. However, I am not certain about the long term. I hope the company can continue to wield its dominant position well and navigate the complicated geopolitical situation carefully.

(D) Is the Stock Cheap?

To answer this question, I turn to my discount cash flow algorithm. First, I estimated the earnings using the company’s historic ROE average of 25%. I then assumed that TSMC pays out 50% of future earnings as dividends and reinvests the rest at constant ROE. I assumed that 10 years down the line, I will be able to sell the stock at a PE ratio of 16, near its historic average.

All these earnings and cash flows were then discounted using a discount rate of 9%, keeping in mind that dividends are taxed at 20% in Taiwan. I arrived at somewhere between US$54 to US$59 a share.

Tweaking the numbers, weighing for different scenarios doesn’t change the final result much. As such, I think the current stock price of $55 is fair. It isn’t particularly cheap.

(E) Is the Manager Track Record Good?

There should be no question about this. It is a resounding yes. A comparison between TSMC and its closest competitors show a stark difference in technology leadership and profitability. This could not have been achieved by accident.

Unfortunately, Morris Chang, the founder who brought the company to such heights, recently retired. I hope that key high level managers are still able to implement his vision and methods. The board members and management team also consist of PhDs and Masters degree holders in related fields, not the typical corporate bean counter types.

Here’s a summary of my checklist.

(A) Is the Company Profitable? – Yes

(B) Are the Profits Real? – Yes

(C) Are the Profits Sustainable? – Medium term yes, long term unsure

(D) Is the Stock Cheap? – No. A fair price.

(E) Is the Manager Track Record Good? – Yes

TSMC is a great company. Today, it is sitting at $55 a share, a price that I think is fair. If it drops below this range, I will be collecting more shares.

I will end off here with a quote from my idol.

It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

Warren Buffett